Distinguished Lecture Series 2024/2025

Electricity price forecasting

Electricity price forecasting (EPF) is a branch of energy forecasting on the interface between econometrics/statistics, computer science and engineering, which focuses on predicting the spot and forward prices in wholesale electricity markets. Over the last 25 years, a variety of methods and ideas have been tried for EPF, with varying degrees of success. In this four part series I will review recent developments in this fascinating area, including (but not limited to) pre- and postprocessing, calibration window selection, probabilistic forecasting, combining forecasts, deep learning, and economic evaluation.

Date, time and venue

- 3 (Mon) and 4 (Tue) March 2025

- Charlotte 🇺🇸: 🕓 15:30-17:30 EST (UTC-5)

- Venue: International Symposium on Energy Analytics (ISEA2025), University of North Carolina at Charlotte 🇺🇸

Recorded videos

Videos freely available on the IIF YouTube channel.

Videos freely available on the IIF YouTube channel.

Part I, Lecture I

Part I, Lecture II

Part II, Lecture I

Part II, Lecture II

Lecture slides & Julia/Python notebooks

Electricity price forecasting I [hyperlinked-PDF 6.2 MB]

- Intro

- Energy forecasting literature

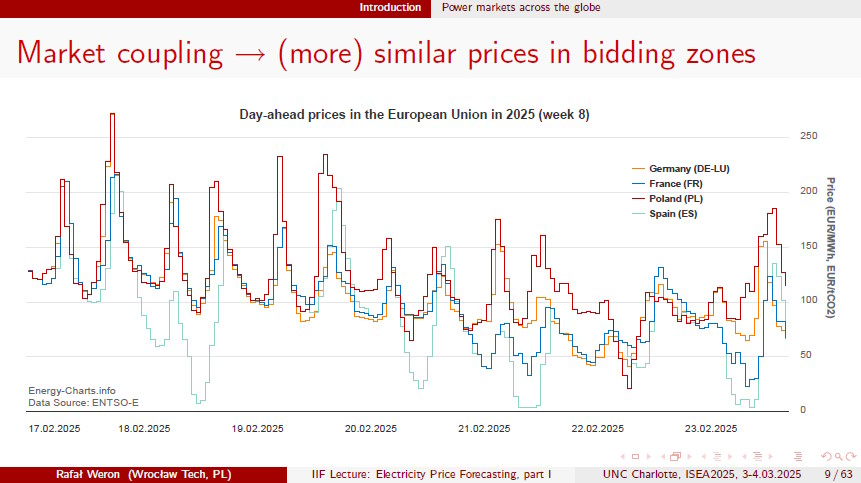

- Power markets across the globe

- Model taxonomy

- 'Toy' models

- The forecasting setup

- Naive models

- (Auto)regressive models

- Nonlinear AR models

- Exponential smoothing models

- Supply stack models

- Beyond point forecasts

- Probabilistic forecasts

- Reliability & sharpness

- Postprocessing point forecasts

- Historical simulation

- Conformal prediction

- Forecast accuracy

- Absolute and square errors

- Percentage errors

- Scaled and relative errors

- Testing for coverage

- CRPS and the pinball score

- DM-type tests

Electricity price forecasting II [hyperlinked-PDF 12.7 MB]

- Tips and tricks

- Transformations

- Seasonal decomposition

- Combining forecasts

- Averaging across calibration windows

- Calibration window selection

- Lasso and DNN

- Stepwise regression

- Shrinkage (regularization)

- LASSO-Estimated AR (LEAR)

- Deeper and deeper

- Interpretable AI

- Probabilistic forecasts revisited

- Quantile Regression Averaging

- Isotonic Distributional Regression

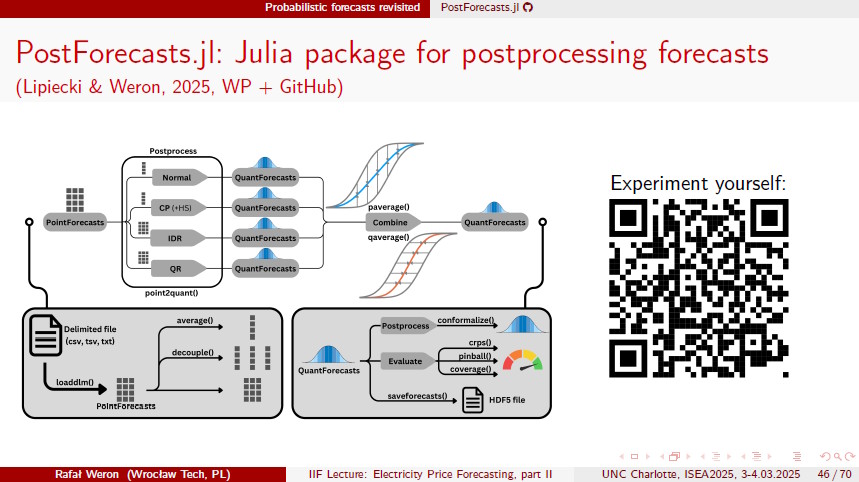

- PostForecasts.jl

- Combining probabilistic forecasts

- Distributional Deep Neural Nets

- Probabilistic inputs

- Financial evaluation

- Day-ahead bidding with BESS

- Which loss function to minimize?

Julia & Python notebooks by Arkadiusz Lipiecki

- Repository with Julia & Python notebooks that illustrate the concepts covered in Rafał Weron's IIF Distinguished Lectures at ISEA2025: GitHub lipiecki/energy-analytics-2025 with

support

support

Software and data

- PostForecasts.jl in Julia (maintained by Arkadiusz Lipiecki) – a package for postprocessing point predictions to obtain probabilistic forecasts. See Lipiecki & Weron (2025, SoftwareX, doi: 10.1016/j.softx.2025.102200) for details. See also Lipiecki et al. (2024, Energy Economics, doi: 10.1016/j.eneco.2024.107934).

- DistributionalNN in Python (maintained by Grzegorz Marcjasz) - library for training, calibrating and making predictions with distributional deep neural networks (DDNN). See Marcjasz et al. (2023, Energy Economics, doi: 10.1016/j.eneco.2023.106843) for details.

- NBEATSx in Python (maintained by Christian Challu) - library that extends the NBEATS model to incorporate exogenous factors (includes a notebook with examples: nbeatsx_example.ipynb). See Olivares et al. (2023, International Journal of Forecasting, doi: 10.1016/j.ijforecast.2022.03.001) for details.

- epftoolbox in Python (maintained by Jesus Lago) - library providing codes for training LEAR and DNN models. See Lago et al. (2021, Applied Energy, doi: 10.1016/j.apenergy.2021.116983) for details. The accompanying market data is here.

- tsrobprep in R (maintained by Michal Narajewski) - package for robust preprocessing of time series data

- IDEAS/RePEc repository in Matlab, Python and/or R - codes for LEAR models, Seasonal Component AutoRegressive (SCAR) models, seasonal decomposition, etc.

2023/2024 edition

- Forecast reconciliation by Rob Hyndman: Over the past 15 years, forecast reconciliation methods have been developed to ensure forecasts are coherent. Forecasts at all levels of aggregation are produced, and the results are "reconciled" so they are consistent with each other. These lectures provide an up-to-date overview of this area, and show how reconciliation methods can lead to better forecasts and better forecasting practices.

- Videos freely available on the IIF YouTube channel.