Conferences

EFC Workshop Series

|

The EFC Workshops are informal meetings devoted to the latest developments in Energy Finance. This highly successful series has had editions since 2011, each set in a different city: Wrocław, Sydney, Oslo, St.Gallen, Paris, Essen, Kraków, Bolzano, Dublin, ... For details see the EFC website. |

ETBI Series

|

ETBI is a series initiated by the Department of Operations Research and Business Intelligence. Its aim is to bring convergence among researchers, academics, and industry experts, facilitate multidisciplinary and interdisciplinary research, and promote the application of emerging technologies in business. For details see the ETBI website. |

Organized events

- "Energy Economics and Forecasting" Session, Modern Electric Power Systems (MEPS'15) Symposium

Venue: Wrocław, 06-09.07.2015

Selected topics: Modeling and forecasting electricity prices, CO2 emissions trading, investments in the power sector, renewable energy - "Statistics in Energy" Session, 12th Workshop on Stochastic Models, Statistics and Their Applications (SMSA2015)

Venue: Wrocław, 16-20.02.2015

Selected topics: Statistical Inference, Time Series Analysis, Stochastic Models in Engineering, Statistical Computing and Simulation, Statistics in Energy (modeling and forecasting electricity prices, CO2 emissions trading, quantitative techniques, renewable energy, electricity price spike forecasting) - CODYM Spring Workshop (CODYM-Spring'14)

Venue: Wrocław, 7-8.04.2014

Selected topics: Cultural and opinion dynamics, complex systems, innovation diffusion, language, linguistics and cognition, social systems and economics - The Energy Finance Christmas Workshop (EFC11)

Venue: Wrocław, 19-20.12.2011

Selected topics: CO2 emissions trading, power market data filtering and deseasonalizing, quantile regression applications, modeling with regime switching models, weather derivatives

Selected talks

|

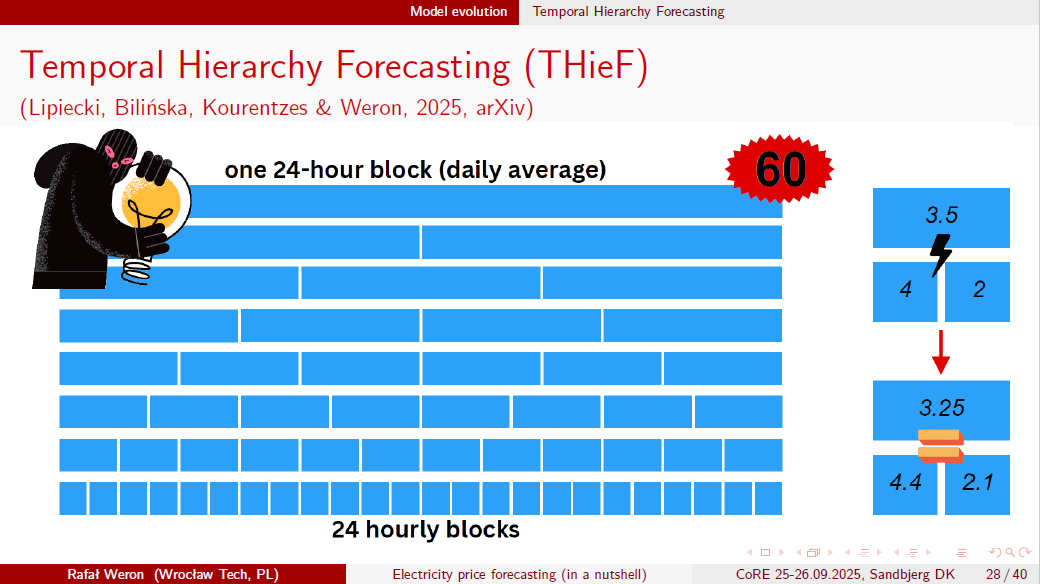

Stealing accuracy: Predicting day-ahead electricity prices with Temporal Hierarchy Forecasting (THieF),

19th International Joint Conference on Computational and Financial Econometrics and Computational and Methodological Statistics (CFE-CMStatistics), Birkbeck - University of London, GBR 🇬🇧, 13-15.12.2025 [hyperlinked-PDF 4.0 MB]

Stealing accuracy: Predicting day-ahead electricity prices with Temporal Hierarchy Forecasting (THieF),

19th International Joint Conference on Computational and Financial Econometrics and Computational and Methodological Statistics (CFE-CMStatistics), Birkbeck - University of London, GBR 🇬🇧, 13-15.12.2025 [hyperlinked-PDF 4.0 MB]

* Earlier version of this talk presented by Arkadiusz Lipiecki at the 14th International Ruhr Energy Conference (INREC), Essen, GER 🇩🇪, 26-27.08.2025. |

|

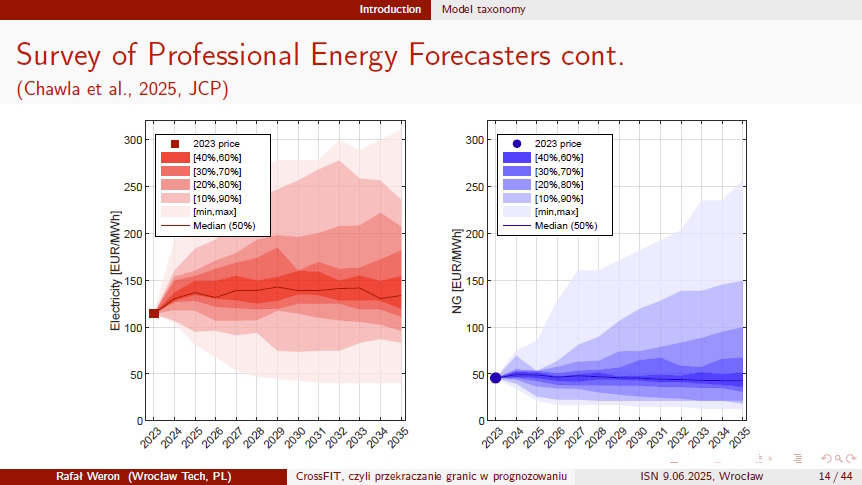

Electricity price forecasting (in a nutshell),

CoRE Members' Retreat, Sandbjerg Gods, DEN 🇩🇰, 25-26.09.2025 [hyperlinked-PDF 9.5 MB]

|

|

Crossing Frontiers in electricity prIce forecasTing (CrossFIT),

Interdisciplinary Scientific Seminar, Wrocław Tech, POL 🇵🇱, 09.06.2025 [hyperlinked-PDF 11.2 MB]

|

|

Recent Advances in Electricity Price Forecasting: A 2025 Perspective,

8th Annual Conference of the Portuguese Association of Energy Economics (APEEN), University of Beira Interior, Covilhã, POR 🇵🇹, 10-11.04.2025 [hyperlinked-PDF 14.1 MB]

|

|

IIF Distinguished Lectures on electricity price forecasting, International Symposium on Energy Analytics (ISEA2025), University of North Carolina at Charlotte, USA 🇺🇸, 3-4.03.2025. See IIF Distinguished Lecture Series 2024/2025

|

|

Recent Advances in Electricity Price Forecasting: A 2024 Perspective, Energy Transition Centre Inaugural Talk, Queensland University of Technology, Brisbane, AUS 🇦🇺, 17.12.2024 [hyperlinked-PDF 9.5 MB]

* Earlier version of this talk presented at the DStatG Statistical Week, Regensburg, GER 🇩🇪, 10-13.09.2024, and the Department of Economics and Finance Seminar, Tor Vergata University of Rome, ITA 🇮🇹, 11.10.2024. |

|

Recent Advances in Electricity Price Forecasting: A 2023 Perspective, Catapult, Value in Energy Data series, GBR 🇬🇧, 29.11.2023 [hyperlinked-PDF 7.7 MB] |

|

Electricity price forecasting in the 2020s (MMXXs), International Conference on Computational Finance (ICCF 2022), Bergische Universität Wuppertal, Wuppertal, GER 🇩🇪, 6-10.06.2022 [hyperlinked-PDF 10.5 MB] |

|

Recent advances in electricity price forecasting: A MMXXII (i.e., 2022) perspective, Applied Machine Learning Days 2022 @EPFL, Lausanne, CHE 🇨🇭, 26-30.03.2022 |

|

Recent advances in electricity price forecasting: A MMXXII (i.e., 2022) perspective, Energy Finance Italia Edizione 7 (EFI7), Parthenope University of Naples, Naples, ITA 🇮🇹, 10-11.02.2022 [hyperlinked-PDF 11.8 MB] |

|

Recent advances in electricity price forecasting: A MMXX (i.e., 2020) perspective, MathSEE Symposium 2020, Karlsruhe Institute of Technology, GER 🇩🇪, 7-9.10.2020 [hyperlinked-PDF 9.1 MB] |

|

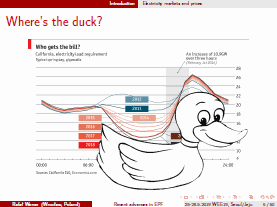

Recent advances in electricity price forecasting: A MMXIX (i.e., 2019) perspective, NBP Workshop on Forecasting, National Bank of Poland (Narodowy Bank Polski, NBP) Warsaw, POL 🇵🇱, 25-26.11.2019 [hyperlinked-PDF 11.2 MB] |

|

Recent advances in electricity price forecasting: A 2019 perspective, 2019 Workshop on Energy Economics: Econometric Analysis of Energy Demand and Climate Change, Seoul & Jeju, KOR 🇰🇷, 25-28.05.2019 [hyperlinked-PDF 7.6 MB] |

|

Recent advances in electricity price forecasting: A 2018 perspective, 7th International Ruhr Energy Conference (INREC2018), Essen, GER 🇩🇪, 24-25.09.2018 [hyperlinked-PDF 6.0 MB] |

|

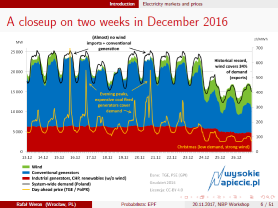

On the importance of the long-term seasonal component in day-ahead electricity price forecasting. Part II - Probabilistic forecasting, Commodity and Energy Markets Annual Meeting (CEMA2018), Rome, ITA 🇮🇹, 20-21.06.2018 [hyperlinked-PDF 2.1 MB] |

|

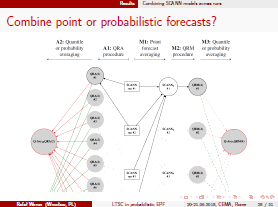

Probabilistic electricity price forecasting (EPF) ... and related topics, NBP Workshop on Forecasting, National Bank of Poland (Narodowy Bank Polski, NBP) Warsaw, POL 🇵🇱, 20-21.11.2017 [hyperlinked-PDF 5.6 MB] |

|

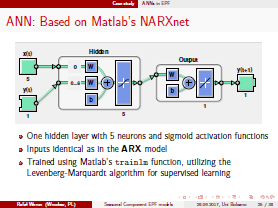

Importance of the long-term seasonal component in day-ahead electricity price forecasting: Regression vs. neural network models, Workshop on Electricity Markets, University of Bolzano, ITA 🇮🇹, 28.09.2017 [hyperlinked-PDF 2.5 MB] |

|

Day-ahead electricity price forecasting with high-dimensional structures: Univariate vs. multivariate modeling frameworks, Department of Economics Seminar, University of Verona, ITA 🇮🇹, 27.09.2017 [hyperlinked-PDF 3.0 MB] |

|

Recent advances in electricity price forecasting (EPF), International Symposium on Energy Analytics (ISEA2017), Cairns, AUS 🇦🇺, 22-23.06.2017 [hyperlinked-PDF 3.0 MB] |

|

Recent trends and advances in electricity price forecasting (EPF), 4th Annual Electricity Price Modelling and Forecasting Forum, Berlin, GER 🇩🇪, 2-3.03.2017 [hyperlinked-PDF 2.6 MB] |

|

Advances in forecasting of wholesale electricity prices, 11th International Summer School on "Risk Measurement and Control" (ISS2016), Rome, ITA 🇮🇹, 6-11.06.2016 [PDF 6.4 MB; revised 25.09.2016] |

|

Two faces of word-of-mouth: Understanding the impact of social interactions on demand curves for innovative products, 80th Annual Meeting of the DPG and Spring Meeting, Regensburg, GER 🇩🇪, 6-11.03.2016 [PDF 1.4 MB] |

|

Probabilistyczne prognozowanie hurtowych cen energii elektrycznej, Posiedzenie Komitetu Statystyki i Ekonometrii (KSiE) PAN, Warszawa, POL 🇵🇱, 8.12.2015 [PDF 3.0 MB]

Probabilistyczne prognozowanie hurtowych cen energii elektrycznej, Posiedzenie Komitetu Statystyki i Ekonometrii (KSiE) PAN, Warszawa, POL 🇵🇱, 8.12.2015 [PDF 3.0 MB]

|

|

Probabilistic forecasting of wholesale electricity prices, 2nd International Conference on Forecasting Economic and Financial Systems (FEFS), CAS, Beijing, CHN 🇨🇳, 30.10-1.11.2015 [PDF 3.5 MB] |

|

A look into the future of electricity price forecasting (EPF), 4th Energy Finance Christmas Workshop (EFC14), St.Gallen, CHE 🇨🇭, 11-12.12.2014 [PDF 1.1 MB] |

|

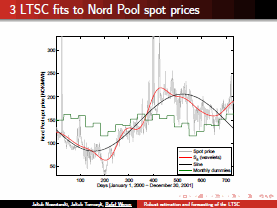

Robust estimation and forecasting of the long-term seasonal component (LTSC) of electricity spot prices, Energy Economics and Finance Seminar, Reykjavik, ISL 🇮🇸, 24-25.05.2013 [PDF 0.5 MB] |

|

A guide to robust modeling of electricity spot prices, Conference on Energy Finance (EF2012), Trondheim, NOR 🇳🇴, 4-5.10.2012 [PDF 2.2 MB] |

|

Modelowanie spotowych cen energii elektrycznej, Seminarium SEFIN, Poznań, POL 🇵🇱, 20.04.2012 [PDF 3.5 MB]

* English language version of this talk (Inference for MRS models of electricity spot prices) presented at the Department of Statistics and Applied Probability Seminar (organized jointly with the Risk Management Institute), National University of Singapore, SIN 🇸🇬, 14.03.2012 [PDF 3.4 MB] |

|

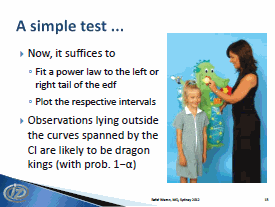

Black swans or dragon kings? A simple test for deviations from the power law, Centre for Financial Risk Seminar, Macquarie University, Sydney, AUS 🇦🇺, 21.03.2012 [PDF 1.8 MB]

* Earlier version of this talk presented at the 47th Winter School of Theoretical Physics "Simple Models for Complex Systems", Lądek Zdrój, POL 🇵🇱, 7-12.02.2011. |

|

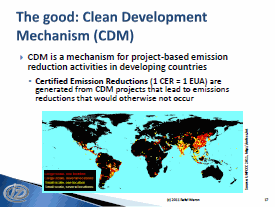

The European CO2 emissions trading system (EU-ETS): The good, the bad and the interesting, Macromodels 2011, Poznań, POL 🇵🇱, 30.11-3.12.2011 [PDF 6.1 MB]

* Second part of this talk presented at the EEM12 Conference, Florence, ITA 🇮🇹, 10-12.05.2012, as The relationship between spot and futures CO2 emission allowance prices in the EU-ETS. |

|

Markov regime-switching models for electricity prices, Financial Mathematics Seminar, University of Sydney, AUS 🇦🇺, 24.08.2010 [PDF 2.9 MB]

* Extended version of this talk presented at the Centre for Financial Risk, Macquarie University, Sydney, AUS 🇦🇺, 18.08.2010. |

|

Regime-switching models for electricity spot prices: An empirical comparison, Conference on Energy Finance, University of Agder, Kristiansand, NOR 🇳🇴, 24-25.09.2009 [PDF 2.6 MB] |

|

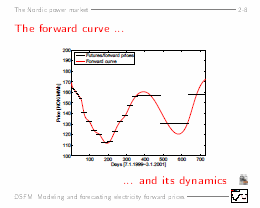

Modeling and forecasting electricity forward prices: A Dynamic Semiparametric Factor Model (DSFM) approach, 2nd AMaMeF Conference "Advances in Mathematics of Finance", Będlewo, POL 🇵🇱, 30.04-5.05.2007 [PDF 1.3 MB, AVI movie 2.3 MB]

* Extended version of this talk presented at the Modelling & Measuring Energy Risk conference, Lisbon, POR 🇵🇹, 14-15.06.2007, as Forecasting spot and forward electricity prices: Semi-parametric time series models. |

|

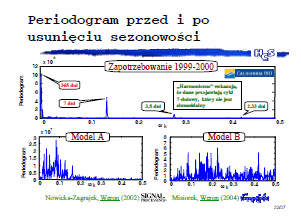

Modelowanie i prognozowanie zapotrzebowania oraz cen energii elektrycznej w warunkach rynkowych, Seminarium Wydziału Elektrycznego PWr, Wrocław, POL 🇵🇱, 6.12.2004 [PDF 1.4 MB]

|

|

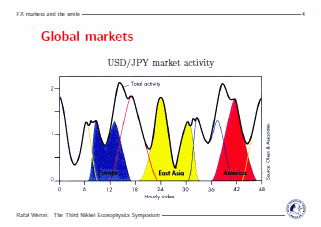

Stochastic volatility model of Heston and the smile, The 3rd Nikkei Econophysics Symposium, Tokyo, JPN 🇯🇵, 9-11.11.2004 [PDF 0.6 MB] |

|

Energy price risk management ... from a three year perspective, XVIII Max Born Symposium, Lądek Zdrój, POL 🇵🇱, 22-25.09.2003 [PDF 3.3 MB] |

|

Everything you always wanted to know about the Levy-stable law, but were afraid to ask, The 2nd ISM/SOKENDAI ECONOMICS Meeting, Institute of Statistical Mathematics, Tokyo, JPN 🇯🇵, 11.11.2002 [PDF 0.9 MB] |